File your s corp election form, and start saving on taxes every single year.

Let us handle your 2553 form for the S corp election

Effortlessly submit your S corp election form (Form 2553) with a user-friendly, precise, and cost-effective solution.

Error-free form 2553

Streamline your S corp election process with an accurate document, making it a breeze.

Correct timing

Even if you missed the deadline, we can still submit your late S corp election and make it right.

Reliable submission

We safeguard your personal information and file your form with the correct department.

Fill out and submit

Having extensive expertise, we have effectively processed and filed numerous S corp elections.

Simplified S-corp election process

Streamlined filing process – file your 2553 form fast and easily.

Futured by following media outlets

How to set up an S corp?

Before setting up an S Corporation (S Corp), you typically need to have a legal entity, LLC or Corporation, in place.

Register your LLC

Registering your sole proprietorship as a single-member LLC can provide you with personal liability protection and additional benefits for your business.

Get your EIN

Obtaining an EIN (Tax ID Number) for your single-member LLC can help fulfill your legal requirements and facilitate banking and tax-related activities.

File your 2553 Form

Filing an S-corp election for your single-member LLC can provide tax benefits and potential savings while maintaining the flexibility of an LLC structure.

What is an S-corp?

An S-corp is a tax-advantaged corporation with limited liability and pass-through taxation.

LLC vs S-cop

LLC offers flexibility but no tax saving benefit. S Corp provides tax advantages and limited liability protection.

Corp vs S-corp

Corporation offers limited liability; S Corp adds tax advantages and pass-through taxation benefits.

Benefits of S-corp

S Corp offers tax advantages, limited liability protection, and potential for easier access to capital.

CPA for S-corp

A CPA or an Enrolled Agent can provide expert guidance on tax compliance and financial strategies for S Corps.

S corp payroll

S-Corp payroll includes officer salary, subject to reasonable compensation guidelines and payroll tax obligations.

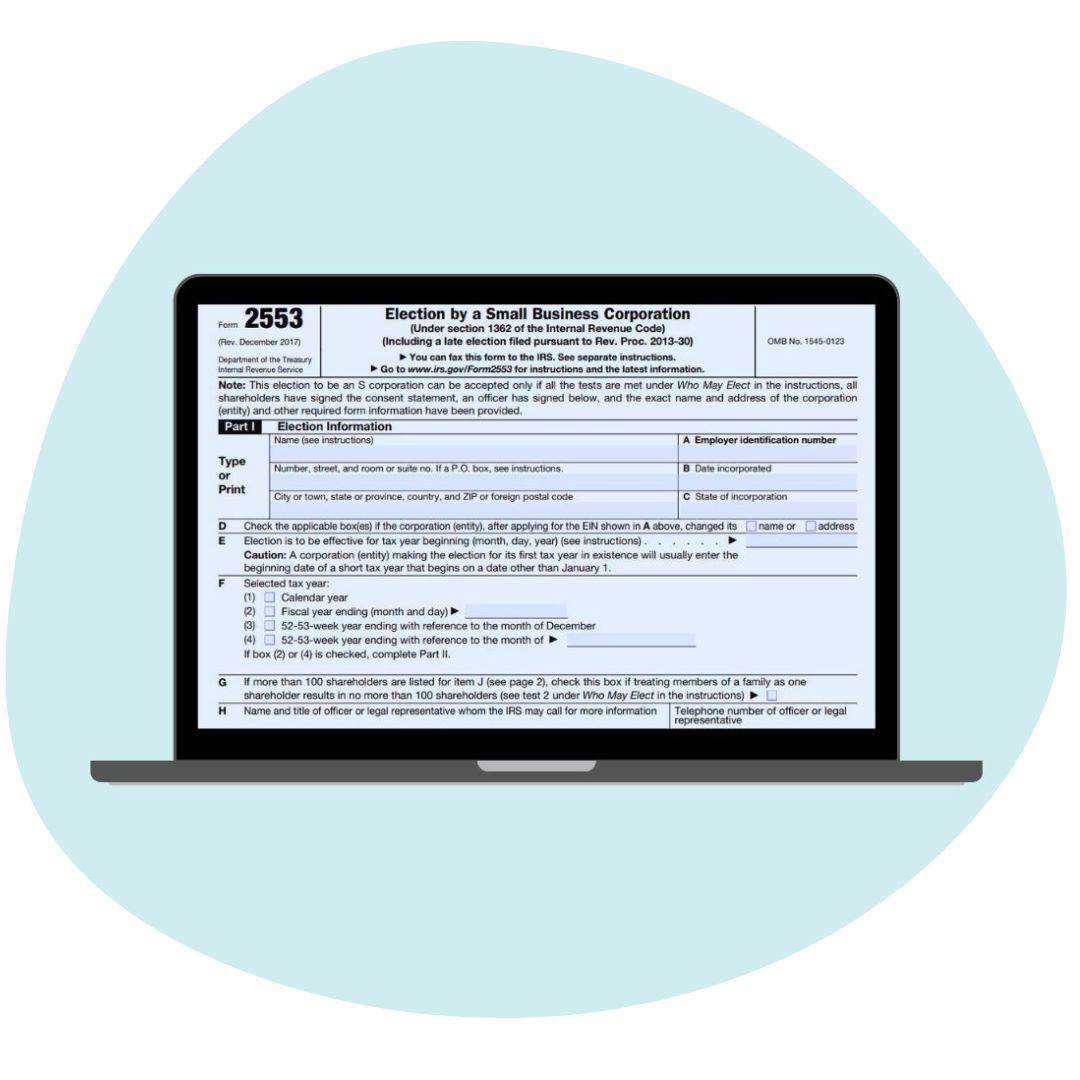

IRS Form 2553

The 2553 Form is used to elect S Corp status for a corporation or LLC with eligible shareholders for potential tax-saving benefits.

Form 8832

The 8832 Form, also known as "Entity Classification Election," is used to change the tax classification of an eligible entity.

How to elect to be an S-Corp?

Key steps for S-Corp election and filing Form 2553.

Step 1.

Provide entity information

Enter the entity’s name (e.g., ABC LLC), address, and EIN.

Step 2.

Choose effective date

Specify the desired effective date for S Corp status.

Step 3.

Identify tax year

Indicate the entity’s tax year (usually calendar year).

Step 4.

Authorized representative

Designate an authorized representative for the entity.

Step 5.

Sign and date

Sign and date the form, indicating the capacity in which you are signing.

Step 6.

Shareholder information

List all eligible shareholders and their ownership percentages.

Step 7.

Shareholder consents

Obtain signatures of all shareholders consenting to the election.

Step 8.

File the form

Send the completed form to the appropriate IRS address.

FAQ S-Corp election

Can an S corp own an LLC?

Yes, an S Corp can own an LLC. This is known as a subsidiary structure, where the S Corp holds the ownership interest in the LLC while maintaining its separate legal and tax status. The LLC may need to have S-corp status as well to qualify QSub. A qualified subchapter S subsidiary (QSub) is a subsidiary corporation that an S Corporation wholly owns.

Do S-corps get 1099?

No, the S Corporation itself does not receive Form 1099. Instead, the S Corporation’s shareholders may receive Form 1099-MISC or other information returns for the income they receive from the S Corporation, such as distributions or non-employee compensation. The S Corporation is responsible for providing the necessary information to its shareholders for tax reporting purposes.

S corp salary 60/40 rule

The s corp salary 60/40 rule suggests a reasonable salary allocation for S Corp owners, with approximately 60% as salary and 40% as distributions, considering factors like roles, industry standards, and business profitability.

Where to file form 2553?

You must file Form 2553 with the Internal Revenue Service (IRS). The easiest way is to fax the completed 2553 form to the appropriate fax number based on your location:

For U.S. fax numbers:

- Eastern U.S.: (855) 641-6935

- Central U.S.: (855) 641-6934

- Mountain U.S.: (855) 641-6937

- Pacific U.S.: (855) 641-6936

For international fax numbers, you can visit the IRS website or contact the IRS directly for the appropriate fax number based on your location.

Learn more about How to file Form 2553.