As many taxpayers are celebrating the new increase in 2023 standard deductions by the IRS, does it make any good for the people who bought homes recently or planning to buy in 2023?

But first, let’s look at new changes

Taxpayers will get higher deductions as IRS adjusts standard deductions. The standard deduction for married couples filing jointly will be $27,700 in 2023 taxes. That is a $1,800 more deduction compared to the number in the tax year 2022. For those who are single taxpayers and married individuals filing separately, the standard deduction will be $13,850 for 2023, which is $12,950 for 2022. For heads of households, who are unmarried but have at least a qualified child or dependent, the standard deduction will be $20,800 for the tax year 2023, $1,400 more compared with the tax year 2022.

| Filing status | 2021 tax year | 2022 tax year | 2023 tax year |

| Single | $12,550 | $12,950 | $13,850 |

| Married, filing jointly | $25,100 | $25,900 | $27,700 |

| Married, filing separately | $12,550 | $12,950 | $13,850 |

| Head of household | $18,800 | $19,400 | $20,800 |

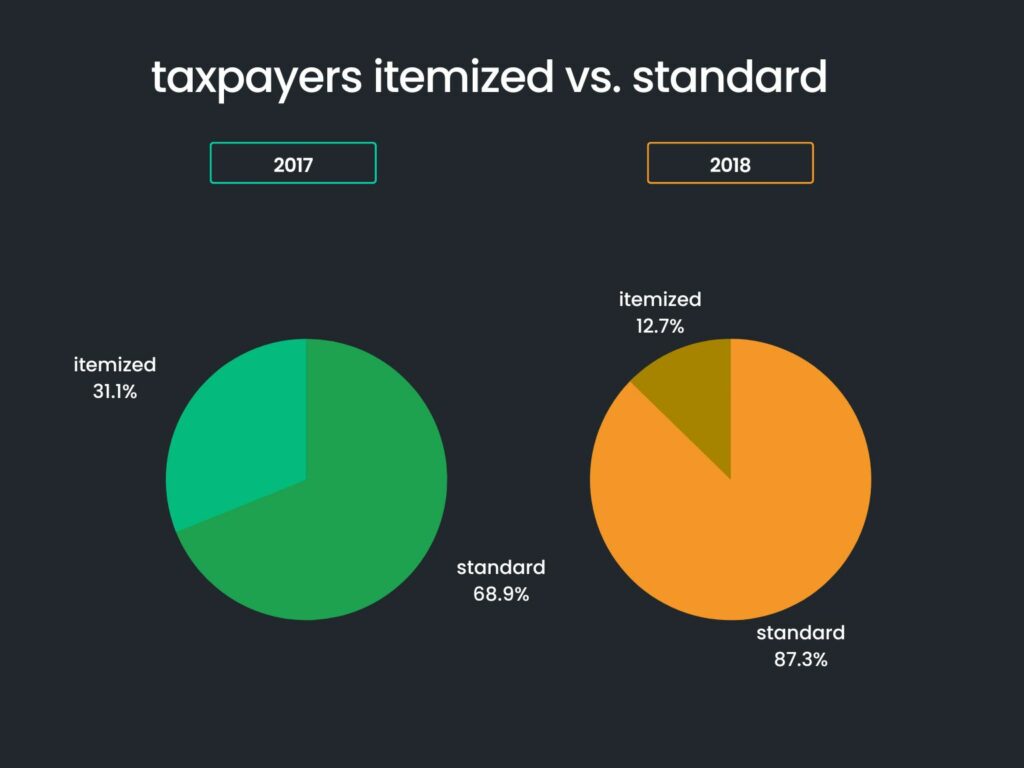

Many people stitched to standard deductions since 2018

The effect of the tax reform was that many people who used to itemize on Schedule A took the standard deduction instead.

According to IRS publications 1304, the standard deduction was taken on 68.9 percent of returns in 2017. However, 87.3 percent of taxpayers claimed standard deductions in 2018. The total amount of the standard deduction claimed for Tax Year 2018 rose 148.5 percent. This increase was due, in part, to the increase in the basic standard deduction and elimination of personal and dependent exemptions under TCJA (Tax Cuts and Jobs Act).

Based on IRS publications 1304

Second, The Tax Cuts and Jobs Act, which was signed into law in 2017, eliminated or limited many itemized deductions.

For example, miscellaneous itemized deductions, such as unreimbursed job expenses, subject to a 2% of AGI threshold went away in 2018. Since then, taxpayers are not able to deduct expenses such as union dues, investment fees, or hobby expenses.

The SALT deduction has become limited to $10,000 ($5,000 if married and filing separately), ($5,000 if married and filing separately).

Another reason that made standard deductions more popular was lower interest rates. Mortgage interest deduction was not enough for many homeowners to claim itemized deductions. TCJA limited mortgage debt limit as well. For any such loan originated after December 16, 2017, the new limit has become $750,000 ($375,000 if married and filing separately). Prior to that date, you could deduct interest on mortgage debt of up to $1 million ($500,000 for married taxpayers filing separately).

For homebuyers in late 2022 and in early 2023

Since the interest rates hit over 7%, many new homebuyers should consider choosing itemized deductions. Even limitations on mortgage debt stay in tax law, taxpayers nowadays are buying homes on a mortgage with higher interest rates (currently over 7%) and can benefit from itemizing their deduction under Schedule A rather than itemizing. For example, only a $500,000 mortgage with current rates can generate over $35,000 in tax deductions on Schedule A. Additionally, a $10,000 SALT deduction ($5,000 if married and filing separately) plus charitable donations will make that number over $45,000. However, the highest new standard deduction for married filing jointly will be only $27,700 in 2023.

More good news for late home buyers

Itemized deductions do not only affect federal tax liability, but they may also reduce state taxes as well. Many states have much lower standard deductions. However, if the deductions are itemized, states pick up the itemized deduction amount from Schedule A of the federal income tax return. Higher itemized deductions on federal tax returns mean lower taxes on state income tax returns as well.

Tax tip for 2023 homebuyers

Tax tip for 2023 homebuyers

Tax tip for 2023 homebuyers

Tax tip for 2023 homebuyersIf you are planning to buy a home in 2023, charitable donations could be a great opportunity to maximize your itemized deductions. Before moving from your current place to your new home in 2023, make sure to donate all your unnecessary furniture, appliances, vehicles, clothes, books, and other household items to a charitable organization and keep all the records for the 2023 tax year.

Charitable contributions include higher limit thresholds after TCJA. Most gifts by cash or check can be up to 60% of your AGI versus the previous limit of 50%. Consider boosting your itemized deductions with charitable donations.