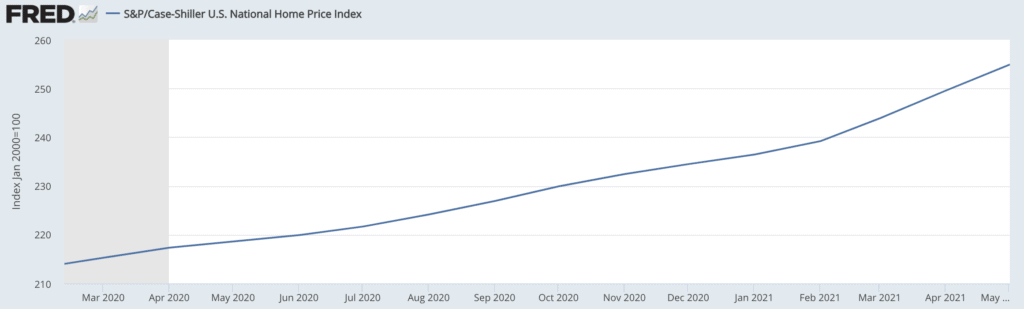

Even though the costs of homes were expected to level out, we have experienced unprecedented rising home prices. From April to May, the year-over-year national average increased from 14.8% to 16.6%. According to Crail J. Lazzara, managing director at S&P Dow Jones Indices pointed out that the 16.6% rise is the highest in over 30 years. Initially, five metro areas recorded an all-time high. These metropolises grew by five more in May. The data for 20 of the top metro areas are recording high price gains based on Case-Shiller data.

What is Case-Shiller?

The U.S. National Home Price NSA Index looks at the 20 largest metro areas in the US. Data are compiled to obtain a three-month moving average. Metro areas are comprised of urban and suburban counties to create one metropolitan statistical area or MSA. The moving average looks at the past few months, so the figures are a bit behind. Over the last 14 months, the metrics are rising non-linearly.

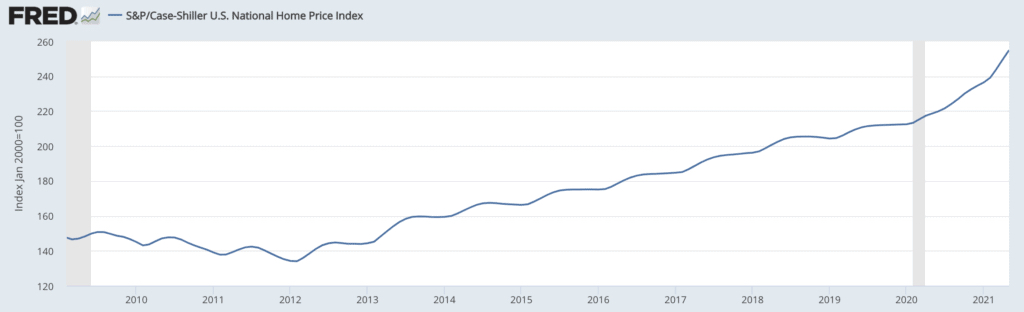

Compare these metrics to the widened view of the 12 years after the Great Recession we experienced in 2007 to 2009:

What are the takeaways?

Throughout202, we witnessed a steady rise that is substantial as well as sustainable. Interest rates were low and personal incomes and job growth continued to grow. As Millennials started hitting their prime home-buying years, the supply of available homes for sale remained low. The pillar metrics can no longer keep up with rising averages of selling prices. Interest rates can’t realistically go much lower. It became apparent as long ago as May that the metrics were moving in the wrong direction.

Due to slightly lower mortgage rates and rising incomes, the median home-buying power rose less than 10% last year. But that’s nothing if you compare it to the over 16% rise in average selling prices.

Where do we put the blame?

Hopefully, some of the factors causing rising home prices will soon be history. The pandemic is one of the largest factors. As COVID-19 surged, many families began to move from city-dwelling to suburban living. The Zoom economy took off as employers eagerly transitioned to work-from-home. Once CPVID-19 is not a national health concern, will the WFH trend continue? As companies continue to choose work-from-home arrangements, more families are encouraged to seek homes in more rural and suburban areas.

The Economical Effect of Rising Home Prices

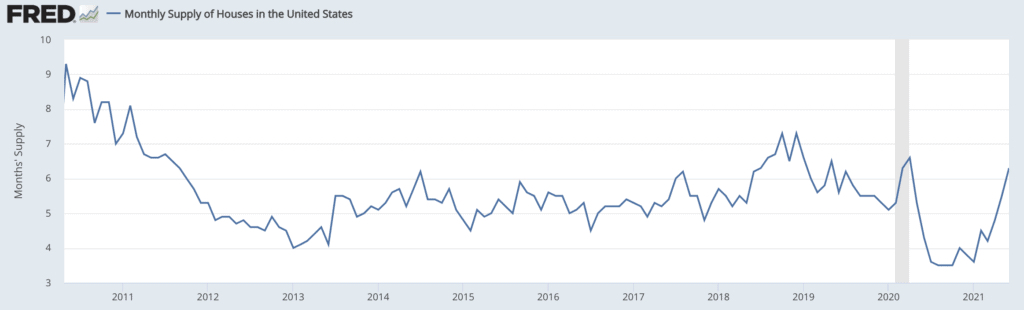

When home prices rise too quickly, people stop buying. Most become content with renting and choose to wait for prices to come down. But things are different than when it all crashed from 2007 to 2009. Mortgages are no longer issued unless income is verified. Other governmental regulations and standards help provide a protective firewall. As a result, June was the third month in a row where prices declined. Sales reported are significantly down from expectations. This downward trend demonstrates the deterioration of total home sales.

Is there any hope?

For those who hope to see an increase in new-home construction, lumber prices have fallen by more than 50% over the last few months. Other factors like the prices of copper derivatives, labor, and shortages of molded fixtures have dissipated to help encourage new construction. Still, there’s a huge drop in building permits which reached a 9-month low earlier this year. Even with these positives, new properties are not being developed fast enough to meet the need of Millennial buyers, especially as remote workers seek larger homes located outside of metro areas.

Unprecedented Times

Image by F. Muhammad from Pixabay

COVID-19 has no modern precedent. We do not know how this move from the city to the suburbs will affect our economy, especially in a digital market. There’s also no precedent for the interventions and stimulus that have been handed out over the last couple of years. Who knows how it will affect mortgage rates or inflation? Now is not the time to try to build your portfolio with incremental properties. Homes are not likely to act like other asset classes. You can expect to see a plateau where overall sales slow down until inventories can begin to keep up with the demand again. That will likely take from 12 to 18 months due to the lag times in construction.